Non-traditional credit documents can strengthen mortgage approval

According to the data from the 2019 Home Mortgage Disclosure Act (HMDA) 8.9% of mortgage applicants (about 1.3 million people) were denied. The number one reason for denial is a high debt-to-income ratio, followed by “credit history.”

Although the majority of consumers have a credit score, there are many with minimal credit experience or have no score at all.

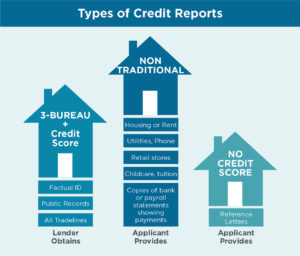

“Non-traditional credit” is an alternative set of verification steps and documentation standards that help support loan approval. Such standards meet the underwriting requirements of Fannie Mae, Freddie Mac, FHA, VA and Rural Housing. The infographic summarizes three types of credit verifications:

3-Bureau + Score describes the mortgage lender’s first step to validate the factual ID of each individual on the loan application, check public records, and obtain the current status and payment history of all debts, known as trade-lines.

Non-traditional verifications consist of information obtained by the lender as well as supplemental documents furnished by the applicant. There are a number of everyday expenses that are not reported to credit bureaus (unless there is a delinquency) that can strengthen a credit file if applicants can substantiate a 1- to 2-year satisfactory payment history. Sources may include: landlords, utility companies, cable television, cell phones, health insurance, auto insurance, union dues, equipment leases, and payments made for child care or long-term medical expenses.

No Credit Score often represent consumers with no credit cards or no checking/savings account. Some first-time homebuyers are living with family members and therefore have no history of paying rent or utilities. Such applicants can strengthen their credit profile by providing signed letters of reference from credit sources that describe the financial relationship and payment history. On-going household expenses that are paid in cash can be documented with paper receipts or photo images of receipts.

The most important thing potential homebuyers can do is to be vigilant in keeping all financial records. Even if bills are paid electronically, banks and credit card companies provide monthly statements (as well as year-end summaries) that can be printed or downloaded.

The above illustration and best practices are adapted from Chapter 5, Credit and Credit Scores, in my book, Housing Finance 2020 (Hipoteca 2020 in Spanish).